5% Good Advisors | 90% Salespeople

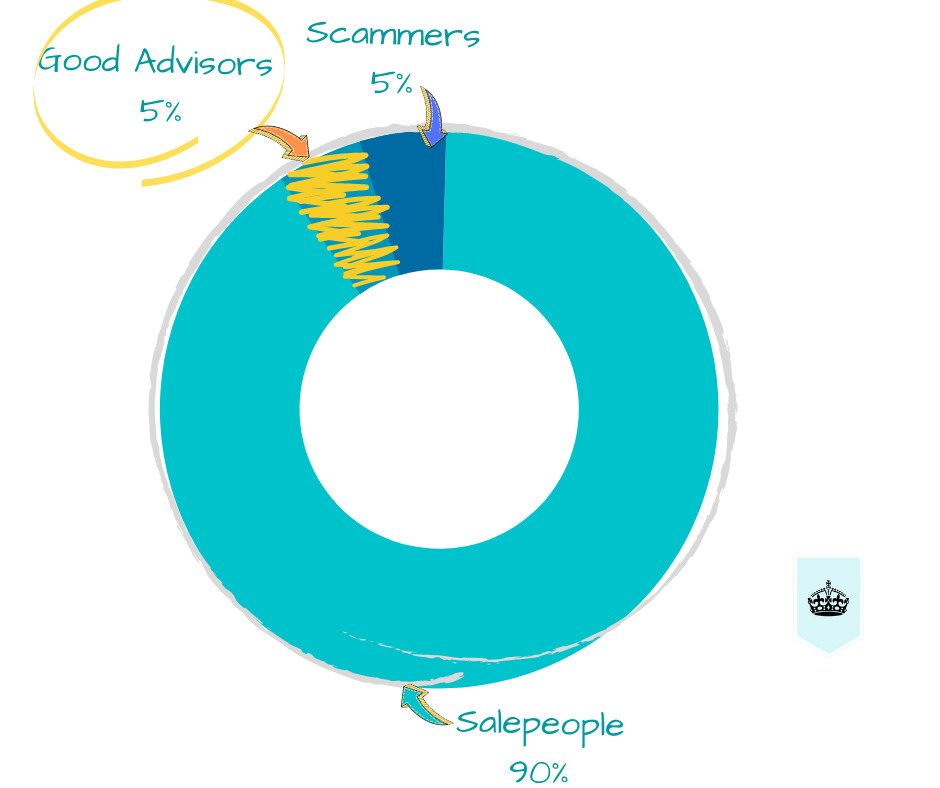

Advisors often face a conundrum, “are you in it for the money” or “are you out to do good for the masses”. But 5% of Advisor choose neither of these options!

Advisors often face a conundrum, “are you in it for the money” or “are you out to do good for the masses”.

Whether you agree with this or not, 100% of Advisors start their career as Salespeople,

about…