The Four-Step Repricing Sequence That Doesn't Move Your Clients

Revenue Acceleration Intelligence: Your Fee Was Set by Rumor and Maintained by Inertia

Answer honestly: where did your fee schedule come from?

For most Financial Advisors, the true answer is archaeology. The schedule was inherited from the practice you joined, or copied from whatever the established firm across town was believed to charge, or set years ago at a number that felt defensible and has not been seriously examined since. It was shaped by a survey summary glimpsed in a trade article, a custodian conference slide, and the folk wisdom that “everyone charges about one percent.” The single number with the most leverage over your revenue, your margins, and your enterprise value was set by rumor, and it is maintained by inertia.

This is not a personal failing. It’s really a structural one. You cannot price against a market you cannot see, and advisory pricing is genuinely invisible. Your competitors do not publish what clients actually pay. Industry surveys report what Advisors say they charge, in aggregates too broad to locate your specific market and segment. Even the client sitting across from you, quoting what some other firm supposedly charges, is usually repeating a half-remembered number from a first meeting. Nearly every participant in the fee conversation is negotiating from folklore and hearsay.

Today’s briefing is about what that blind spot costs, the partial fixes most Advisors attempt, and the public data source, sitting in plain sight at the SEC, that ends the rumor era entirely for practices equipped to use it.

What Folklore Pricing Actually Costs

Start with the dispersion the “everyone charges one percent” myth conceals. Kitces Research, the most rigorous ongoing fee research in the profession, finds that the familiar median holds: roughly 100 basis points on portfolios up to a million dollars, declining on graduated schedules as assets grow. But the median is not the market. The same research shows that even the unremarkable middle of the profession, the 25th through 75th percentile of blended AUM fees, spans roughly 100 to 120 basis points on sub-million-dollar portfolios. The middle half of the industry disagrees with itself by twenty basis points, and the full range beyond that band is wider still, with plenty of Advisors above 120 on smaller relationships and high-net-worth medians drifting toward 50 basis points.

Now run the arithmetic on your own book, because this is where the blind spot converts to dollars. Let’s look at a scenario where this Advisors is handles $60 million in advised assets, twenty basis points is $120,000 a year. That is the annual revenue difference between sitting at the bottom and the top of the ordinary middle of the market, before anyone does anything exceptional. An Advisor priced fifteen basis points below their justified position on that book forgoes $90,000 every year, roughly the fully loaded cost of the Associate Advisor or Operations Director they keep deciding they cannot afford. Underpricing does not show up as a line item. It shows up as the hire not made, the capacity ceiling hit early, and the enterprise value multiple applied to a smaller revenue base at exit.

The second cost is defensive discounting against a threat that the real data says is exaggerated. The compression story is like industry wallpaper: robo-advisors, index funds, and AI planning tools are supposedly grinding advice fees toward zero. Kitces Research has repeatedly found the opposite in the numbers: standalone planning fees, retainer fees, and hourly rates have all risen meaningfully over its survey cycles, and AUM fees have held remarkably stable, even firming at the affluent end. Yet Advisors who cannot see across the market shave basis points at the first sign of resistance anyway, negotiating against a rumor of compression rather than the fact of stability. When you cannot verify your position, every objection sounds credible.

This is what the Chairman’s Council Revenue Acceleration Intelligence exists to do, replace the industry’s folklore with its data, decoded for Advisors building toward seven figures. Upgrade to premium membership to read the full repricing playbook below.

The Partial Fixes, and Why They Stay Partial

Advisors who take pricing seriously usually reach for one of four approaches, and each helps while falling short of the same standard: verified, current, local, disclosed truth.

Industry surveys are the most common. They are genuinely useful for national context, but they are self-reported, aggregated across wildly different markets and service models, and published on a lag. A national median cannot tell you what the five firms your prospects actually compare you against are charging. Custodian benchmarking is a step closer, but it sees only the firms on that custodian’s platform and typically reports at a level of aggregation designed to avoid revealing anyone. Study groups offer real candor about real numbers, but a sample of eight friendly practices is anecdote wearing a data costume. And pricing consultants can be excellent, but they deliver an episodic snapshot at consulting prices, and the market keeps moving after the engagement ends.

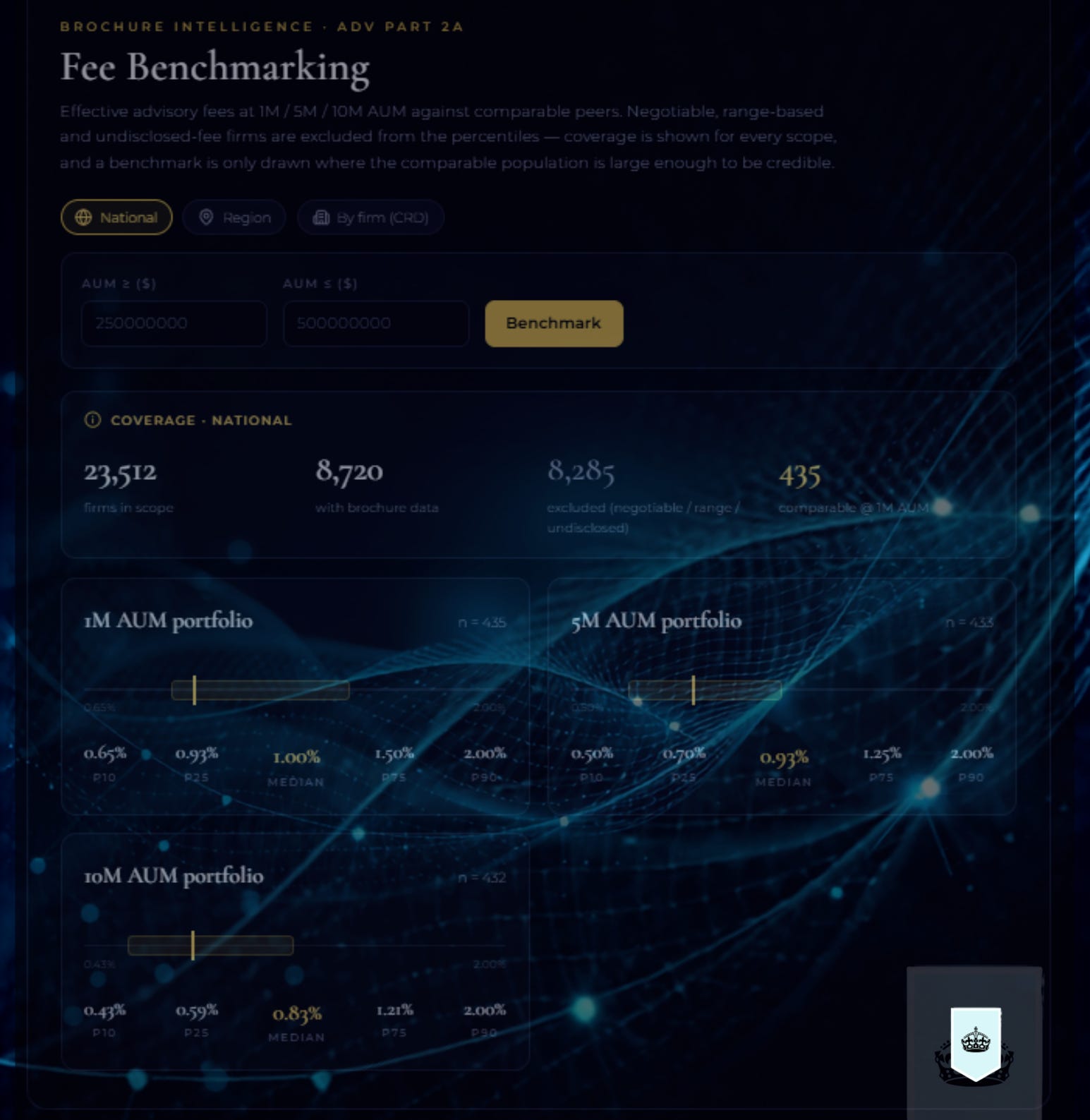

Here is the strange part. The verified version of this data has been public the entire time. Every SEC-registered investment adviser is required to disclose its fee schedule and compensation structure in Form ADV Part 2A, the plain-English brochure filed with the regulator, and those filings are publicly available through the SEC’s Investment Adviser Public Disclosure system. Not what firms tell a survey. What they disclose, under regulatory obligation, in a document their compliance officer signs off on. The disclosed pricing of your actual competitive landscape is sitting on a government website right now.

So why does folklore still rule? Because the disclosure infrastructure was built for regulation, not comparison. The answer is scattered across thousands of narrative PDF brochures in inconsistent formats, and no practicing Advisor has the hours to read, extract, and structure their market’s filings, then keep the picture current as firms amend. The data exists. The structure does not. That gap, between public truth and usable truth, is exactly the kind of gap this publication exists to point at, and closing it is what the rest of this briefing covers: the system that turns regulator-filed fee data into a pricing position you can defend to the basis point, and the four-step playbook for converting that intelligence into revenue.

Below the paywall: how filings-based fee intelligence actually works, the four-step repricing sequence, the positioning percentile we hold premium practices to, and the conversation frameworks for moving your fee without moving your clients — become a premium member to continue.

The Edge: Pricing From Filings While Competitors Price From Rumor

This is the capability we rebuilt Synseus’ benchmarking around (here). The platform’s fee and valuation benchmarks are constructed from SEC IAPD and Form ADV Part 2 filings data: the fee schedules firms actually disclose to their regulator, structured into comparable form, so an Advisor can see where their pricing genuinely sits within their market and segment rather than where a survey summary guesses it sits. To be clear about what is and is not being claimed, this is disclosed schedule data, the pricing architecture firms publish under regulatory obligation. It will not show you the one-off discount a rival quietly gave their largest client. What it shows you is the thing folklore never could: the verified, documented pricing structure of the competitive landscape you are actually operating in.

Think about what changes in each of the moments that used to run on rumor. A prospect says another firm quoted them less: you now know whether that is consistent with anything that firm has ever filed. You are considering a fee increase: you now know whether the move takes you from the 45th percentile to the 60th, or off the map. You are writing your own ADV amendment: you now know how your disclosed schedule will read next to the firms yours will be compared against. Your competitors are making these same decisions on gut feel. That asymmetry is the edge, and it compounds with every pricing decision you make from here forward.

The Four-Step Repricing Sequence